The greatest misunderstanding on finance Twitter is central bank lingo. For the past decade and a half tweeps have been yelling that quantitative easing QE is going to cause hyperinflation and the end of the US Dollar. None of these doomsday predictions have materialized. That is because their understanding of monetary policy is entirely wrong.

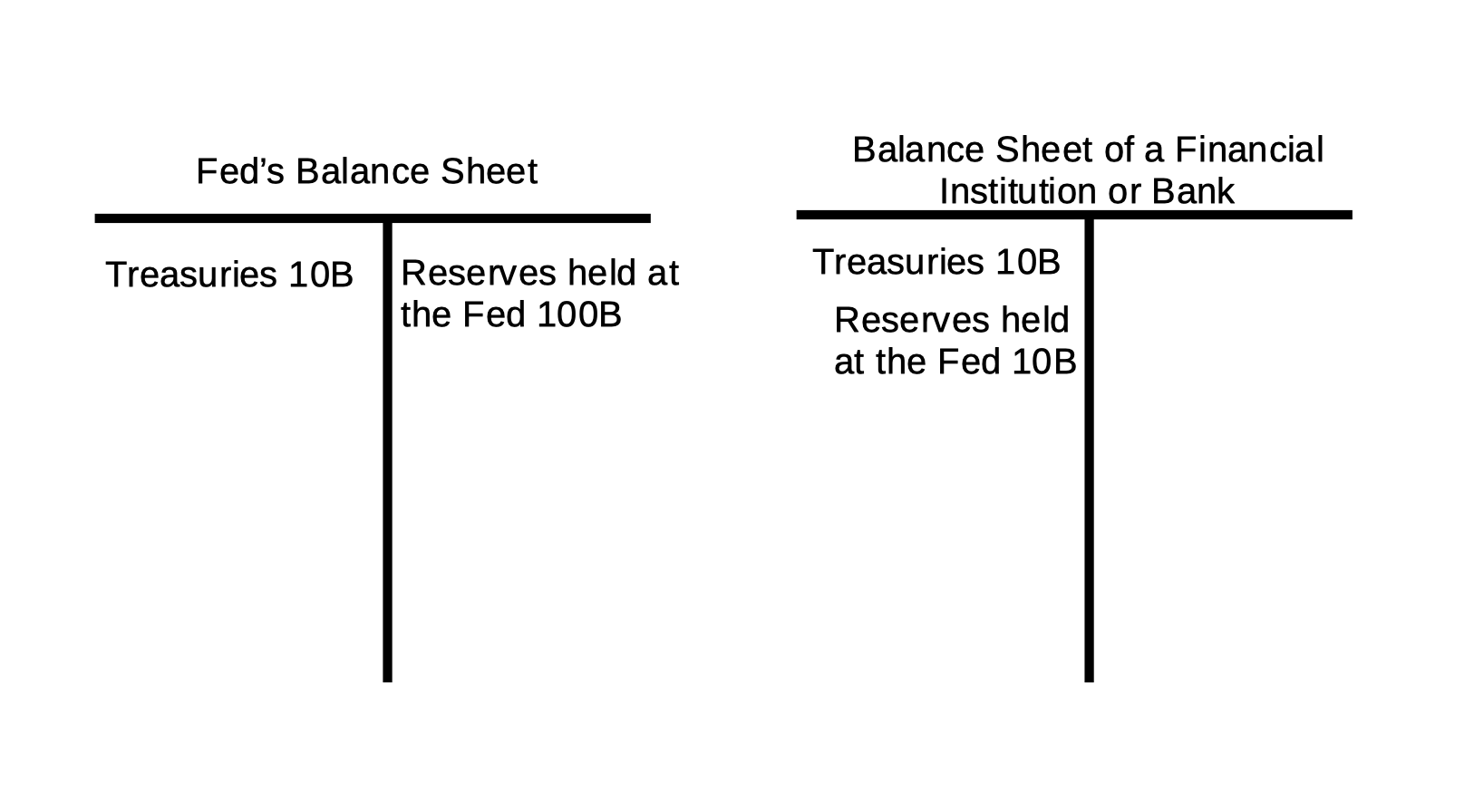

QE is really nothing more than a balancesheet swap operation for major financial institutions. The operation removes from the financial system the same amount of assets valued in dollars that it adds. Therefore it is a net zero for inflation. Banks must maintain a legal minimum amount of reserves with the Federal Reserve. After the Great Financial Crises QE was deployed to boast bank reserves by draining toxic mortgages from the financial system. Here’s how the swap works. The Fed credits the reserve account of a financial institution Dollars in exchange for a financial insititution’s mortgages or treasuries. The Fed then keeps theses mortgages and treasuries on its own balance sheet until they reach maturity and rollover or sells them back into the market before then.

Imagine the Fed’s balance sheet and a balance sheet at a typical financial institution. The Fed may want to derisk financial markets by draining toxic or underwater mortgages like it did after 2008. Maybe a financial institution wants to strengthen their reserves during a recession or meet reserve requirements.

In 2008 the Fed introduced an interest rate on reserves balance, IORB. to encourage banks to cushion their risk further. Furthermore reserves held at the Fed cannot be used to purchase risk assets such equities (otherwise they wouldn’t be reserves anymore lol). Therefore we can debunk the disinformation that QE inflated the broader stockmarket and created wealth inequality.

Money is created through fiscal spending via the Treasury. Excessive fiscal policy, often untargeted, can contribute to demand side inflation. Still most inflation is created by us the consumer, whenever we expand our own balance sheets, and by business activity. The market is a function of our own bidding and asking not the Fed propping up the market.

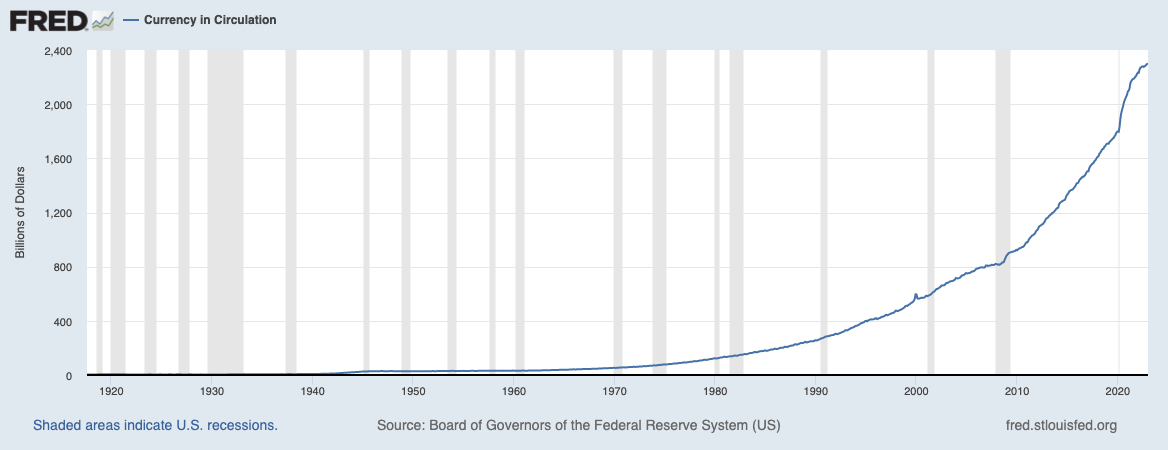

Finally the St. Louis Monetary Base is really just a representation of excess reserves that banks hold at the Fed added to the amount of currency in circulation. For myself I find the St. Louis Monetary Base calculation nonsensical and just adds confusion for the general public. Bank reserves do not circulate in the economy they remain parked at the Fed earning a smol IORB.

To prove one more time that QE isn’t inflationary we can take examples highlighted in Mark’s tweet verbatim. All of these demonstrate that QE is just an asset swap between central banks and financial institutions.

Finally the only effect QE has on the market is one of pure psychology and ideology. Most traders believe the Fed is propping up the financial markets via these operations. This can be relayed back the the Taper Tantrum which came to a head in 2018 when financial markets derisked. This time the effect isn’t as significant it seems.